It is said that 23% of seniors will not tolerate loss in their retirement savings. Are you one of them? If so, your retirement plan may be ineffective—which is why it will help to get a risk evaluation ASAP.

Whether you are aware of it or not, behavioral finance biases can wreak havoc on your retirement plans. Yes, your brain can influence your investment account, and loss aversion is one of the most common pitfalls when it comes to how you spend and invest your money. So, understanding yourself in relation to your wealth can play a vital role in your overall financial success.

Learn how social behavior and rational decisions go hand-in-hand, by working with a dedicated financial advisor in Norman, OK.

At the heart of this matter is what we know and appreciate as socionomics. This article will help you understand how loss aversion can steer you in the wrong direction when it comes to retirement planning in Norman, Oklahoma, and what you can do about it.

What is loss aversion and how does it impact retirement planning?

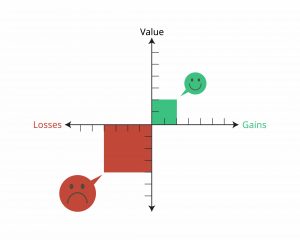

Fear resides at the core of loss aversion. When you think about how your parents were raised and what financial struggles they endured, you may see a relative trend. And because it is common to fear losing money rather than staying hopeful about growing wealth from diverse investments, you might make some financial decisions that lead you to miss out on opportunities.

Coming to terms with loss aversion bias can be done with a financial advisor who understands it well. They will be able to alter a skewed portfolio to include a healthy amount of risk, which will be based on your risk tolerance (your ability to handle potential losses) and time horizon (when you need the funds).

Extreme Loss Aversion

People who cling to their money may be experiencing extreme loss aversion. Some of their thoughts may include:

- My family is telling me to play it safe.

- I have had a bad investment experience.

- This is all the money I have.

- I don’t understand how to invest.

- I don’t understand volatility and loss.

- I don’t know who I can trust.

A non-action safeguard of funds like this can be like a financial life sentence. It may help to remember that depletion of principal reduces your income in the future, which you must rely on for the rest of your life. So, if you’re living on saved-up cash, you will lose money every month.

How to work around the effects of loss aversion in your retirement planning

If you are accustomed to seeing the markets increase over time, repeatedly, you may not perceive those wins as emotional happiness. You have come to expect it, right? But if you check the market and your accounts have plummeted because of volatility, your loss aversion may initiate negative emotions.

If you are accustomed to seeing the markets increase over time, repeatedly, you may not perceive those wins as emotional happiness. You have come to expect it, right? But if you check the market and your accounts have plummeted because of volatility, your loss aversion may initiate negative emotions.

A reaction like this might cause you to pull out of your investments in panic. This is what we want you to avoid. Learning when to buy or sell is the name of the game and one that we at TRAC Advisory Group Inc. are very familiar with.

This is where it pays to understand socionomic theory on a deeper level.

What is Socionomic Theory?

Socionomics examines social mood and its impact on social attitudes/actions and inspects how social mood regulates overall societal behavior. Socionomic theory suggests that leadership and policies are powerless to change it and that their actions as a whole express social mood versus regulating it.

Since stock market indexes can reflect almost instant changes in the social mood, socionomic studies use them as benchmark social-mood indicators, like a sociometer, to anticipate and understand changes in social activity. For example, a more positive society produces more upbeat actions, such as an expanding economy, a rising stock market, and brighter themes in entertainment. An unhappy society would manifest more negative social actions, like a contracting economy, falling stocks, and darker themes across popular entertainment.

How you can reduce the impact of loss aversion on your retirement plan

You may be able to lower the impact of loss aversion on your retirement plan by:

- Not holding on to things with emotional value

- Not beating yourself up over past mistakes

- Being resilient to previous financial loss

- Not straying from your established financial plan

- Admitting when you’re wrong in regards to investments

Working with a financial advisor can help hold you accountable for your financial behavior tendencies. Thinking before you act is key. That’s why it will help to ask yourself a hand-full of questions to get to the root of your financial tendencies.

Five questions to ask yourself to help you understand how loss aversion may be impacting your retirement plan

In order to see where loss aversion might be impacting your retirement plan, it can help to ask yourself these questions, for starters:

In order to see where loss aversion might be impacting your retirement plan, it can help to ask yourself these questions, for starters:

- Am I holding onto investments that keep losing value because I don’t want to sell below a given amount?

- Am I putting off uncomfortable conversations around long-term care, legacy planning, and disability?

- Do I have sentimental value attached to possessions or investments that were gifts?

- Am I operating fearfully and missing out on opportunities based on a negative past experience, like a market crash?

- Am I choosing unwise risks to try to counteract existing losses?

Resources to help you further explore retirement planning in Norman OK

Behavioral economics provides a framework to comprehend why someone delays investing in a retirement account even if they understand the power of compounding interest. This can be a good place to start.

Ask a fiduciary financial advisory firm specializing in behavioral finance, we can help you get past this roadblock. There’s no shame in doing what you were taught. But when we learn more about ourselves, and how we can improve, it helps to have a financial guide.

Work with a socionomic aware investment manager at TRAC, to steer clear of behavioral tendencies holding you back from retirement success.

Three Takeaway Tips

- Take a good look at long-term market data: events like recessions and bubble bursts have created temporary speed bumps in the growth of the market.

- Think carefully about your true long-term risk tolerance: a <free risk evaluation> (link to the landing page when published) can stress test your portfolio in order to make appropriate adjustments.

- Take a look at your holdings with fresh eyes with the help of a financial advisor in Norman, OK.

Call TRAC for a risk assessment today.

This blog contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass.

Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security.

TRAC Advisor Group does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance.